Case study 01 · Empirical foundation

Bitcoin Market

Dynamics Analysis

An empirical investigation of price dynamics, return distributions and market participation signals in Bitcoin from 2012 to 2022.

Question

What must a useful market model be able to reproduce?

Before building the simulation, I established the empirical behaviour it needed to explain: recurring departures from a long-run value trend, extreme return events, persistent volatility and changes in active wallet counts.

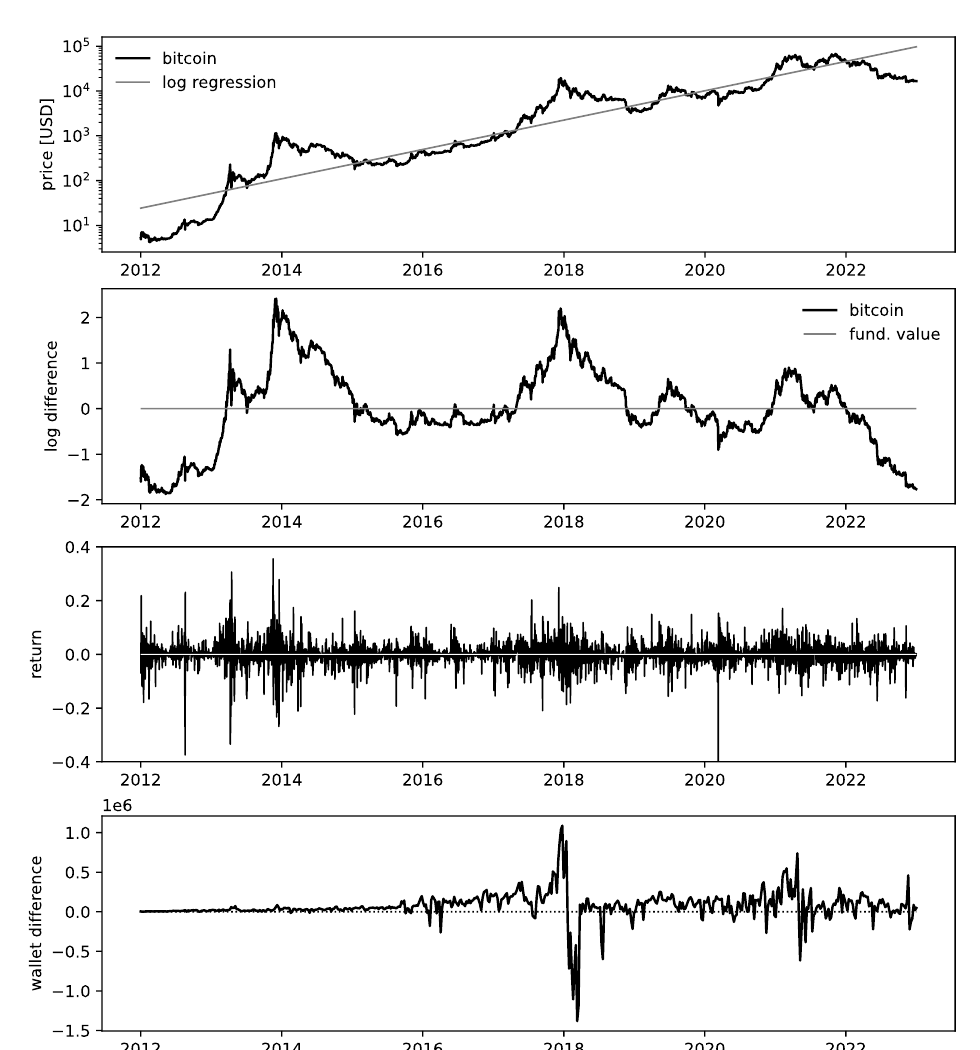

Selected findings

The market is not well described by a smooth equilibrium path.

- Large deviations recur. Price repeatedly moves far above and below its long-run trend.

- Extreme moves matter. Returns show heavy tails, making a normal-distribution assumption insufficient.

- Volatility clusters. Quiet periods and turbulent periods appear in persistent sequences.

From measurement to mechanism

These patterns became the validation target for the agent-based model.

The next case study turns the observed dynamics into a behavioural system: savers, fundamentalists and technical traders can switch strategies as relative performance changes, creating endogenous inflows and outflows.

Explore the agent-based modelContext: Independently authored research and engineering project, developed as a B.Sc. Economics thesis at Leipzig University.