Case study 02 · Systems modelling

Agent-Based

Market Simulation

A behavioural simulation that asks how changing market participation and strategy shifts can produce boom-and-bust cycles without an external shock.

Model

Three behaviours, one evolving market.

The model introduces savers alongside fundamental and technical traders. Savers participate when market strategies outperform saving; traders can switch strategy through relative performance and social interaction. Their changing mix feeds back into price formation.

Result

Participation dynamics create regime shifts.

- Inflows are endogenous. Strategy performance can draw savers into the market and amplify prevailing dynamics.

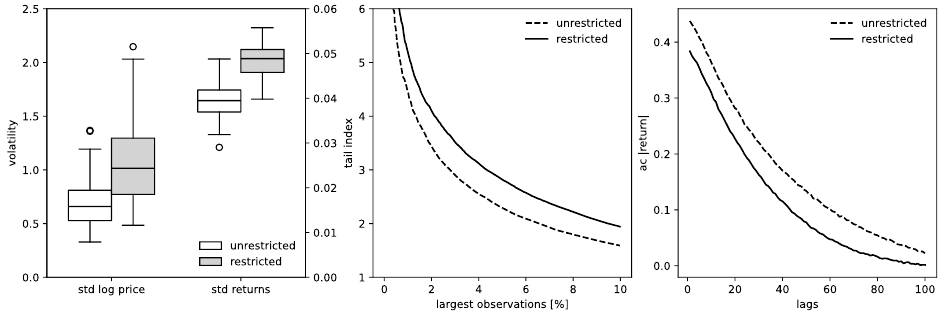

- FOMO raises volatility. Restricting new entrants to trend-following behaviour produces stronger price variability.

- The model is empirically grounded. Distributional and temporal properties are compared against the Bitcoin analysis.

Interactive model

Explore the system directly.

Adjust a small set of meaningful parameters in a dedicated NetLogo Web simulation and observe how the agent population, market flow and price path respond.

Open the simulationContext: Independently authored research and engineering project, developed as a B.Sc. Economics thesis at Leipzig University.